What is the greek called Delta in options trading? How does options delta affect my options trading?

Options Delta - Definition

Options Delta is the options greek that measures the sensitivity of an option's price to a change in the price of the underlying stock.

Options Delta - Introduction

Perhaps the most exotic thing you would ever learn in options trading are the options greeks.

In layman terms, delta is that options greek which tells you how much money a stock option will rise or drop in value with a $1 rise or drop in the underlying stock, which also translates to the amount of profit you will make when the underlying stock rises. This means that the higher the delta value a stock option has, the more it will rise with every $1 rise in the underlying stock. Stock options with options delta of 0.7 is expected to rise $0.70 with a $1 rise in the underlying stock. Stock options value is affected most by changes in the price of the underlying stock, making delta value of stock options the single most important options greeks to understand in options trading.

Where To Get Delta of Options?

You can get the delta value, as well as of other options greeks, from a kind of options chain known as a "Pricer", which is available on all reputable online options brokers. Below is an example of an options pricer taken from Optionsxpress.com.

Options Delta - Characteristics

Positive & Negative Options Delta Values

Options delta values are either positive or negative. Call Options have positive delta values suggesting that it will gain in value proportionately with a gain in value in the underlying stock. Put Options have negative delta values suggesting that it will lose value as the underlying stock rises. Conversely, call options with its positive delta values drops in price as the underlying stock falls and put options with its negative delta values gains in price as the underlying stock falls. In short, positive delta value becomes profitable as the stock goes up and negative delta value becomes profitable as the stock goes down.

Options Delta & Options Moneyness

Options delta value rises as options gets more and more In The Money (ITM) and reduces as the options gets more and more Out Of The Money (OTM). At The Money Options, no matter call or put options, have delta value of 0.5, suggesting a 50% chance of either ending up In The Money or Out Of The Money. Learn about Options Moneyness now.

Options Delta & Time to Expiration

When there is lesser time to expiration, the chances of options staying in their prevailing state of moneyness by expiration increases. This means that the nearer to expiration an option is, the more likely it is that in the money options will stay in the money by expiration and out of the money options staying out of the money by expiration. As such, the nearer to expiration, the higher the options delta value of in the money options would be and the lower the delta value of out of the money would be at the same strike price. Learn about Options Expiration now.

Rate Of Change Of Options Delta

Options delta value changes as it gets more and more in the money or out of the money. This rate of change is governed by another options greeks known as Gamma.

Options Delta - What It Suggests

There are 2 main ways to look at what options delta mean. It is first an indication of how much the value of the option will move with a $1 move in the underlying stock (all else equal, disregarding volatility), secondly, it is also an indication of the approximate probability that the option will end up In The Money (ITM) by expiration. Options with delta value of 1 is pricing in a 100% probability of ending up In The Money by expiration. Options with delta value of 0.5 is pricing in a 50% probability of ending up In The Money by expiration.

Options Delta - An Indication Of Relative Change

The most direct and important application of options delta is in its indication of relative change against the price of the underlying stock. A positive options delta value means that the option's price moves in the same direction as the underlying stock while a negative options delta value means that the option's price moves inversely proportionate to the movement of the underlying stock. When you buy call options, which has positive options delta values, you make money when the stock goes up and loses money when the stock goes down in the same proportion. When you buy put options, which has negative options delta values, you make money when the stock goes down and loses money when the stock goes up.

When you buy call options, you are buying

positive options deltas while you are buying negative options deltas when you buy put options. Conversely, when you

write call options, you are gaining

negative options deltas while you are gaining positive options deltas when you write put options.

| Type | Delta value | Profits When... |

| Long Call Option | Positive | Stock Goes Up |

| Short Call Option | Negative | Stock Goes Down |

| Long Put Option | Negative | Stock Goes Down |

| Short Put Option | Positive | Stock Goes Up |

Delta value also allows you to calculate an approximate gain or loss in value with a $1 move in the underlying stock. If you buy 1 contract of call option with delta value of 0.7, it means that every option gains approximately $0.70 in value when the underlying stock goes up $1. Since 1 contract represents 100 shares, each contract of those call options gain $70 with a $1 gain in the underlying stock. Similarly, if you buy 1 contract of put option with delta value of 0.7, you make $70 for every $1 drop in the underlying stock. These calculations are only approximations because delta value is changing all the time even while the stock is moving and that options prices are also affected by implied volatility.

Since options delta value is the ratio of how much options will move in relation to the underlying stock, delta value suggests how many

corresponding stocks you are effectively buying with those options. 2 contracts of at the money call options with delta value of 0.5 has a total

of 200 x 0.5 = 100 deltas. 100 deltas means that you are effectively controlling the exact movements of 100 shares of the underlying stocks and

therefore almost as good as buying 100 shares (when the underlying stock rises $1, the options rise a total of $100). If you buy 10 contracts of

put options with delta value of -0.75, you are effectively short 1000 x 0.75 = 750 shares. With this in mind, you would be able to calculate the

exact number of options to buy in order to be effectively long or short a definite number of shares. If you wish to be long 1000 shares, you

could either buy 20 contracts of at the money call options with delta value of 0.5 (1000 / 50 = 20) or you could buy 13 contracts of in the

money call options with delta value of 0.77 (1000 / 77 = 13).

Another important application of knowing the exact delta value and thus how much the options will move in relation to its underlying stock

is that it allows you to calculate the exact number of options you need to perform

delta neutral hedging. By having a delta neutral position,

you ensure that the value of your position remain stagnant no matter which way the underlying stock went and is useful when market conditions

are temporarily dangerous.

Options Delta - Probability Of Ending In The Money

Another way of looking at options delta is that it approximates the probability that the option will end up In The Money by expiration. Deep in the money options have delta value of 1 or close to 1, which means that it has almost a 100% chance of staying in the money by expiration. At the money options have delta value of 0.5 or 50%, which means that it has a 50/50 chance of ending in the money by expiration as the stock could move either higher or lower than that price.

For example, if you speculate a 50% chance of a stock rallying, you would buy call options on that stock with no less than an implied 50% chance of ending in the money or delta value of at least 0.5 and above.

Typical Options Delta Values

Even though exact options delta values can only be derived with precise calculation using an options pricing model such as the Black-Scholes Model, experienced options traders usually approximate these values using the following rule of thumbs:

1. At The Money options have options delta value of 0.5.

3. Next Deeper In The Money Options have options delta value of close to 0.9.

5. Nearest Out Of The Money Options have options delta value of close to 0.25.

6. Next further out of the money options have options delta value of close to 0.1.

7. Far Out Of The Money Options have options delta value of close to 0.

|

Please note that this is only a very rough approximation for the purpose of quick reference. If you need precise delta values for hedging or precise trade management, you would need to use the Black-Scholes Model. |

| Strike Price | Call Options Delta | Put Options Delta |

| 15 | 1 | 0 |

| 20 | 0.9 | -0.1 |

| 25 | 0.75 | -0.25 |

| 30 | 0.5 | -0.5 |

| 35 | 0.25 | -0.75 |

| 40 | 0.1 | -0.9 |

| 45 | 0 | -1 |

Factors Affecting Options Delta

2 main factors influence the value of options delta; Time to expiration and Options Moneyness. We have discussed the effects of Options Moneyness on Options Delta value extensively above. In general, Options Delta increases as options go more and more in the money and decreases as the options go more and more out of the money. Options Delta of In The Money options also increases as expiration approaches and the options delta of out of the money options decreases as expiration approaches. Thinking in terms of options delta representing the probability of ending in the money upon expiration, it is not hard to understand why the options delta of in the money options approaches 100 as expiration nears and why options delta of out of the money options approaches 0 as expiration nears.

Knowing that nearer term in the money stock options have a higher delta value than longer term options of the same strike price allows you to

choose the correct option in order to optimize profits for your expected holding period. If you expect a stock to rally within a few days,

you would buy nearer term options instead of longer term options in order to return a higher profit on the same move of the underlying stock.

|

Example : Assuming XYZ company trading at $30 on 1 Jan 2008. Its Jan expiration $25 strike price call options have delta value of 0.75 and

its March expiration $25 strike price call options have delta value of 0.7. Assuming XYZ rises to $32 within 2 days. Jan $25 Call rises by : $2 x 0.75 = $1.50 Mar $25 Call rises by : $2 x 0.7 = $1.40 |

Calculating Aggregate Options Delta

When you have a portfolio with many different stock options positions on a single stock, it is useful to know whether the value of your portfolio will go up or down with a move in the underlying stock. It is also useful to know if your portfolio will do well or not when the overall market goes up or down. You do this by aggregating the total options delta in your portfolio. In general, when the overall market is bullish, your portfolio would do well if it has a positive aggregate options delta and when the overall market is bearish, your portfolio would do well if it has a negative aggregate options delta. Aggregate Options Delta is also known as Position Delta.

Calculating aggregate options delta is very simple. You simply list out all the delta value of all options in your portfolio and sum them

together will do.

| Sample Options Trading Portfolio 1 | |

| Option Position | Delta |

| 2 contracts of XYZ $25Call | 140 |

| 10 contracts of XYZ $60Put | -200 |

| Aggregate Options Delta | -60 |

In Sample Options Trading Portfolio 1, the portfolio would profit if XYZ shares falls because it has an aggregate options delta of -60, which is a negative value.

Because most stocks rise when the overall market rises and fall when the overall market falls, knowing the aggregate options delta of your

overall portfolio gives you an indication as to the market inclination of your portfolio.

| Sample Options Trading Portfolio 2 | |

| Option Position | Delta |

| 2 contracts of XYZ $25Call | 140 |

| 10 contracts of XYZ $60Put | -200 |

| 10 contracts of ABC $20Call | 500 |

| 4 contracts of KKK $80Call | 280 |

| Aggregate Options Delta | 720 |

Sample Options Trading Portfolio 2 has a positive aggregate options delta value of 720, which means that the portfolio can be expected to do well when the overall market rises. Understanding the aggregate options delta value of your portfolio lets you know when to make adjustments when market conditions changes.

|

|

Most online broker interfaces does this aggregation of total portfolio delta for you so you don't have to calculate this yourself. |

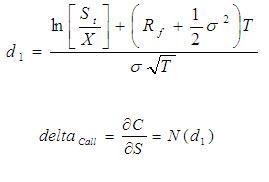

Options Delta Formula

The formula for option delta is:

Where...

C = Value of the Call Option

St = Current value of underlying asset

N(d1) = Rate of change of the option price with respect to the price of the underlying asset

T = Option life as a percentage of year

ln = Natural log of

Rf = Risk free rate of return

Options Delta Questions

:: "Can Options Delta Move Over 1?"

:: "What Is The Difference Between Beta and Delta?"

:: "Do Near Term or Long Term Options Move More?"

Important Disclaimer : Options involve risk and are not suitable for all investors. Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither www.optiontradingpedia.com, mastersoequity.com nor any of its data or content providers shall be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon. Data is deemed accurate but is not warranted or guaranteed. optiontradinpedia.com and mastersoequity.com are not a registered broker-dealer and does not endorse or recommend the services of any brokerage company. The brokerage company you select is solely responsible for its services to you. By accessing, viewing, or using this site in any way, you agree to be bound by the above conditions and disclaimers found on this site.

Copyright Warning : All contents and information presented here in www.optiontradingpedia.com are property of www.Optiontradingpedia.com and are not to be copied, redistributed or downloaded in any ways unless in accordance with our quoting policy. We have a comprehensive system to detect plagiarism and will take legal action against any individuals, websites or companies involved. We Take Our Copyright VERY Seriously!

Site Authored by