How Does Short Calendar Straddle Work in Options Trading?

Short Calendar Straddle - Introduction

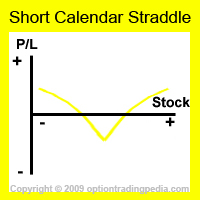

The Short Calendar Straddle is a volatile options strategy designed to profit when a stock is expected to stage a breakout in either direction.

The Short Calendar Straddle produces this effect by selling a long term straddle while buying a short term straddle. No matter which direction the stock breaks out, extrinsic value of all options involved would diminish as they go more and more in the money and out of the money. In this case, profit is made through the difference between the extrinsic value on the short long term options made and the loss of extrinsic value of the long short term options.

|

|

When To Use Short Calendar Straddle?

One could use a Short Calendar Straddle when the underlying stock is expected to breakout strongly to upside or downside quickly.

How To Use Short Calendar Straddle?

Short Calendar Straddles simply consist of a near term long straddle and a longer term short straddle. This means writing longer term at the money call and put options while buying the same amount of nearer term at the money call and put options.

Buy Short Term ATM Call + Buy Short Term ATM Put + Short Long Term ATM Call + Short Long Term ATM Put

|

Short Calendar Straddle Example :

Assuming XYZ trading at $44. It is February and XYZ is awaiting an important court verdict in March. Its Jun44Call is quoted at $2.10, its Jun44Put is quoted at $2.00, its Mar44Call is quoted at $1.00 and its Mar44Put is quoted at $0.80. Sell To Open QQQQ Jun44Call, sell To Open QQQQ Jun44Put Buy To Open QQQQ Mar44Call, buy To Open QQQQ Mar44Put |

Profit Potential of Short Calendar Straddle:

The Short Calendar Straddle profits primarily from the diminished extrinsic value of the long term short options as they go in the money and out of the money as the stock breaks out. Intrinsic value losses are fully hedged by the short term long options, as such, the maximum profit of the short calendar straddle is the difference between the extrinsic value of the long term options and short term options, which is the net credit received initially less residual extrinsic value.

Maximum loss occurs when the underlying stock remained stagnant and closed at the strike price of the options involved. When this happens, the short term long options expires worthless, losing more money than the long term options can compensate through time decay gains. The value of the long term options at expiration of the short term options can only be calculated using an options pricing model such as the Black-Scholes Model.

Profit Calculation of Short Calendar Straddle:

Maximum Profit = net credit - residual value

|

Short Calendar Straddle Example :

Assuming XYZ rallies to $64. Its Jun44Call is quoted at $20.01, its Jun44Put is quoted at $0.01, its Mar44Call is quoted at $20.00 and its Mar44Put is quoted at $0.00. |

|

Short Calendar Straddle Example :

Assuming XYZ falls to $24. Its Jun44Call is quoted at $0.01, its Jun44Put is quoted at $20.01, its Mar44Call is quoted at $0.00 and its Mar44Put is quoted at $20.00. Net Profit: $2.30 - (($20.01 + $0.01) - ($20.00 + $0.00)) = $2.29. |

As you can see from the examples above, the Short Calendar Straddle makes the same maximum profit no matter which direction the underlying stock breaks out.

|

Short Calendar Straddle Example :

Assuming XYZ remains stagnant at $44. Its Jun44Call is quoted at $1.90, its Jun44Put is quoted at $1.95, its Mar44Call is quoted at $0.00 and its Mar44Put is quoted at $0.00. |

As you can see above, the expected loss of a Short Calendar Straddle is lower than its maximum profit potential, putting the odds in your favor.

Risk / Reward of Short Calendar Straddle:

Maximum Profit: Limited.

Maximum Loss: Limited.

Break Even Points (Profitable Range) of Calendar Straddle:

Breakeven points of Short Calendar Straddle can only be determined through the use of an options pricing model such as the Black-Scholes Model.

Advantages Of Short Calendar Straddle:

Disadvantages Of Short Calendar Straddle:

Alternate Actions for Short Calendar Straddle Before Expiration :

1. The moment the extrinsic value of the long and short term options are almost completely eroded due to a significant breakout, the position should be closed and profit taken. There is no need to hold til expiration because the engine that makes this options trading strategy work is the breakout, not time decay.

|

Don't Know If This Is The Right Option Strategy For You? Try our Option Strategy Selector! |

| Javascript Tree Menu |

Important Disclaimer : Options involve risk and are not suitable for all investors. Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither www.optiontradingpedia.com, mastersoequity.com nor any of its data or content providers shall be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon. Data is deemed accurate but is not warranted or guaranteed. optiontradinpedia.com and mastersoequity.com are not a registered broker-dealer and does not endorse or recommend the services of any brokerage company. The brokerage company you select is solely responsible for its services to you. By accessing, viewing, or using this site in any way, you agree to be bound by the above conditions and disclaimers found on this site.

Copyright Warning : All contents and information presented here in www.optiontradingpedia.com are property of www.Optiontradingpedia.com and are not to be copied, redistributed or downloaded in any ways unless in accordance with our quoting policy. We have a comprehensive system to detect plagiarism and will take legal action against any individuals, websites or companies involved. We Take Our Copyright VERY Seriously!

Site Authored by