What is Theta in options trading? What is the effect of Theta on options and what is the characteristics of Theta?

Options Theta - Definition

Options Theta measures the daily rate of depreciation of a stock option's price with the underlying stock remaining stagnant.

Options Theta - Introduction

In layman terms, Theta is that options greek which tells you how much an option's price will diminish over time, which is the rate of time decay of stock options. Time decay is a well known phenomena in options trading where the value of options reduces over time even though the underlying stock remains stagnant. Time decay occurs because the extrinsic value, which is also known as the Time Value, of options diminishes as expiration draws nearer. By expiration, options would have completely no extrinsic value and all Out Of The Money (OTM) Options would expire worthless. The rate of this daily decay all the way up to its expiration is estimated by the Options Theta value. Understanding Options Theta is extremely important for the application of options strategies that seeks to profit from time decay.

Options Theta - Characteristics

Positive & Negative Options Theta Values

Options Theta values are either positive or negative. All long stock options positions have negative Theta values, which indicates that they lose value as expiration draws nearer. All short stock options positions have positive Theta values, which indicates that the position is gaining value as expiration draws nearer.

Options Theta value is highest for At The Money (ATM) options and progressively lower for In The Money (ITM) and Out Of The Money (OTM) as ITM and OTM options have much lower extrinsic values, giving little left to decay. Learn all about Options Moneyness.

Different For Call & Put Options

At the money call and put options sharing the same strike price and expiration date has different theta values. Unlike delta where it is the same 0.5 for both at the money call and put options, Option Theta varies according to the cost of carry of the underlying stock.

Options Theta - Who Should Be Concerned?

Options Theta is an extremely important measurement for the execution of Theta based neutral options strategies that aim to profit from the decay of extrinsic value or Time Decay. Such options trading strategies include the well known Calendar Call Spread and all its variants. Options traders utilizing such options trading strategies must make sure that the aggregate theta values of those positions are positive in order to turn a profit.

Conversely, Options Theta is a lot lesser of a concern for anyone utilizing directional options trading strategies such as Bull Call Spreads where a position is held all the way to expiration. In this case, Options Delta and Gamma would take centre stage instead. These kind of options traders simply take the entire extrinsic value as an expense and build it into the calculation for breakeven point, therefore, how fast that extrinsic value erodes away becomes of secondary concern.

Options Theta - An Indication Of Time Decay

Options Theta measures exactly how much money an option will lose with the underlying stock remaining stagnant on a daily basis. An option contract with Options Theta of -0.012 will lose $0.012 every day even on weekends and market holidays. This is why options traders utilizing neutral options trading strategies love to put on these positions ahead of long weekends where they get 3 safe and free days of decay profits. Conversely, this works against the trader who bought those stock options. If those options contract has options theta of -0.012 and a price of $1.40, the holder will come back after a 3 days long weekend to find the price of those options at $1.36 instead.

Time decay always work against buyers and benefits writers of options. This is because both long call and long put options produces negative Options Theta. Negative options Theta diminishes the price of the options and consequently the value of the position. Many options trading strategies sells out of the money options on top of buying at the money or in the money options in order to partially offset the negative theta, resulting in a lower rate of time decay. An example of such an options trading strategy is Bull Call Spread.

| Type | Theta value | Effect Of Time Decay... |

| Long Call Option | Negative | Negative |

| Short Call Option | Positive | Positive |

| Long Put Option | Negative | Negative |

| Short Put Option | Positive | Positive |

Options Theta - Relationship with Options Gamma

Options Theta is directly proportional to options gamma. The higher the Gamma, the higher the Theta. High risk = high gains. High options gamma results in exponentially higher profits when the stock moves strongly but comes also with higher theta which decays the price of the option much faster. If that anticipated big move does not happen quickly, the option could lose a lot of money. Therefore, when one chooses such an aggressive option position, one must also take into consideration the higher risk involved due to higher Options Theta. Such balancing of potential risks over potential reward is actually prevalent in every aspects of options trading. There is never a free lunch.

Factors Affecting Options Theta

2 main factors influence the value of options Theta; Time to expiration and Options Moneyness. In general, Options Theta decreases as options go more and more in the money (ITM) / out of the money (OTM) and is highest when at the money (ATM). Options Theta also increases as expiration approaches.

Knowing that nearer term at the money stock options have a higher Theta value than longer term options of the same strike price allows you to choose the correct option in order to optimize profits for your expected holding period. If you expect the stock to move but not anytime soon, you should buy options that is as far from expiration as reasonable so as to reduce the effects of time decay.

Calculating Aggregate Options Theta

When you have a portfolio with many different stock options positions on a single stock, it is useful to know how much your overall portfolio is affected by time decay. You do this by aggregating the total options Theta in your portfolio. When aggregate options theta is negative, you know that your portfolio depends on the market moving very quickly in your favor in order to return a profit and when aggregate options theta is positive, you know that your portfolio will do well if the market remains relatively stagnant.

Calculating aggregate options Theta is very simple. You simply list out all the Theta value of all options in your portfolio and sum them together will do.

| Sample Options Trading Portfolio 1 | |

| Option Position | Theta |

| 2 contracts of XYZ $25Call | -2.4 |

| 10 contracts of XYZ $60Put | 1 |

| Aggregate Options Theta | -1.4 |

|

Most online broker interfaces does this aggregation of total portfolio Theta for you so you don't have to calculate this yourself. |

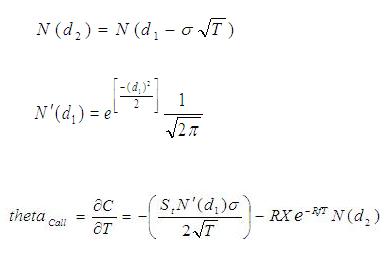

Options Theta Formula

The formula for calculation of option theta is:

Where...

d1 = Please refer to Delta Calculation

T = Option life as a percentage of year

C = Value of Call Option

St = Current price of underlying asset

X = Strike Price

Rf = Risk free rate of return

N(d2) = Probability of option being in the money

Important Disclaimer : Options involve risk and are not suitable for all investors. Data and information is provided for informational purposes only, and is not intended for trading purposes. Neither www.optiontradingpedia.com, mastersoequity.com nor any of its data or content providers shall be liable for any errors, omissions, or delays in the content, or for any actions taken in reliance thereon. Data is deemed accurate but is not warranted or guaranteed. optiontradinpedia.com and mastersoequity.com are not a registered broker-dealer and does not endorse or recommend the services of any brokerage company. The brokerage company you select is solely responsible for its services to you. By accessing, viewing, or using this site in any way, you agree to be bound by the above conditions and disclaimers found on this site.

Copyright Warning : All contents and information presented here in www.optiontradingpedia.com are property of www.Optiontradingpedia.com and are not to be copied, redistributed or downloaded in any ways unless in accordance with our quoting policy. We have a comprehensive system to detect plagiarism and will take legal action against any individuals, websites or companies involved. We Take Our Copyright VERY Seriously!

Site Authored by